您现在的位置是:首页 >技术交流 >[AI学习] 一元线性回归网站首页技术交流

[AI学习] 一元线性回归

一元线性回归

介绍

线性回归(Linear Regression)是一种用于建模和预测变量之间线性关系的统计方法。它假设因变量(目标变量)与一个或多个自变量(特征变量)之间存在线性关系,并通过拟合最佳直线(或超平面)来描述这种关系。

核心概念

1.模型形式

一元线性回归: 只有一个自变量,形式为:

y

=

w

1

x

+

b

y=w_1x+b

y=w1x+b

其中,y是因变量,x是自变量,w1是权重(系数),b是截距

多元线性回归:包含包含多个自变量,形式为:

y

=

w

1

x

1

+

w

2

x

2

+

⋯

+

w

n

x

n

+

b

y=w_1x_1+w_2x_2+⋯+w_nx_n+b

y=w1x1+w2x2+⋯+wnxn+b

其中,

x

1

,

x

2

,

…

,

x

n

x_1,x_2,…,x_n

x1,x2,…,xn是多个自变量,

w

1

,

w

2

,

…

,

w

n

w_1,w_2,…,w_n

w1,w2,…,wn是对应的权重。

2. 目标

找到一组权重 ( w 1 , w 2 , … , w n ) (w_1,w_2,…,w_n) (w1,w2,…,wn)和截距(b),使得模型的预测值和真实值之间的误差最小

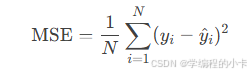

3. 损失函数

用于衡量预测值与真实值的差距:

均方误差(Mean Squared Error, MSE)

其中

y

i

是真实值

y

^

是预测值,

N

是样本数量

其中 y_i 是真实值hat{y}是预测值,N是样本数量

其中yi是真实值y^是预测值,N是样本数量,

4.代价函数

是所有样本误差的平均,也就是损失函数的平均。

5.参数估计

-

梯度下降:通过迭代优化算法逐步调整参数,最小化损失函数。 梯度下降算法(我之前的另一篇)

-

最小二乘法:通过数学推导直接求实例:

假设用面积(x)预测房价(y),模型可能拟合出:

y = 1.2 x + 40 y=1.2x+40 y=1.2x+40

表示每增加1平方米,房价增加1.2万元,基础房价(截距)为40万元。解权重和截距的闭式解。

优缺点:

- 优点:简单、可解释性强、计算高效。

- 缺点:对非线性关系或复杂数据模式拟合能力有限,易受异常值影响

数据集和特征

数据集

定义:数据集是用于训练或测试模型的结构化数据集合,通常以表格形式组织(如 CSV、Excel 文件或数据库表)。每一行代表一个样本(Sample),每一列代表一个属性(即特征或变量)。

数据集的组成

● 样本(Samples):数据集中每一行是一个独立的观测值(如一个用户、一件商品、一条记录)。

● 特征(Features):每一列是描述样本的某个属性(如年龄、温度、像素值等)。

● 标签/目标变量(Label/Target)(监督学习中):需要预测的变量(如房价、分类结果)。

示例

| 面积(平方米) | 房间数 | 楼层 | 房价(万元) |

|---|---|---|---|

| 80 | 2 | 5 | 100 |

| 120 | 3 | 10 | 250 |

| 60 | 1 | 2 | 70 |

- 样本数:3 条(3 行)

- 特征:面积、房间数、楼层

- 标签:房价(目标变量)

数据集的类型

- 结构化数据:表格形式,适合传统机器学习(如房价预测)。

- 非结构化数据:图像、文本、音频等,需转换为特征(如像素、词向量)后使用。

- 时间序列数据:按时间顺序排列(如股票价格、传感器数据)。

特征

定义:特征是描述样本的属性或变量,是模型的输入(自变量)。特征的质量直接影响模型性能。

特征的类型

- 数值型特征(Numerical Features)

○ 连续型:可无限细分(如温度、体重)。

○ 离散型:取整数值(如房间数、点击次数)。 - 类别型特征(Categorical Features)

○ 有序类别:有顺序关系(如评分:高、中、低)。

○ 无序类别:无顺序关系(如颜色、城市名)。 - 文本特征:需转换为数值(如词频、TF-IDF)。

- 时间特征:日期、时间戳(需分解为年、月、日等)。

应用

- 房价预测:

○*特征:面积,地段

○ 标签:房价 - 用户流失预测:

○ 特征:登录频率,使用实操

○ 标签: 是否流失

代码实例

以下代码采用的 python 进行编写

首先需要准备一下数据集

这里我采用的是 kaggle 上面下载的一组数据集,为工作年限与薪资的数据集

https://www.kaggle.com/datasets/abhishek14398/salary-dataset-simple-linear-regression?resource=download

部分数据如下

,YearsExperience,Salary

0,1.2000000000000002,39344.0

1,1.4000000000000001,46206.0

2,1.6,37732.0

3,2.1,43526.0

...

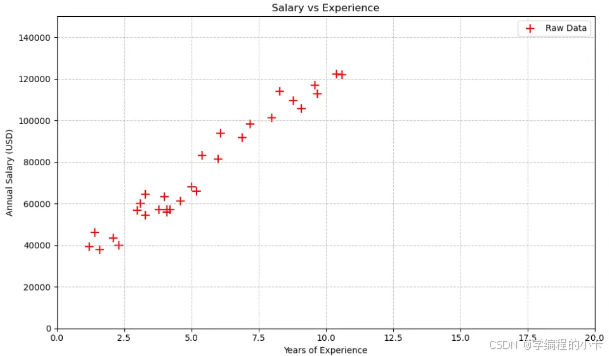

数据图

基于这组数据绘制一下图

import matplotlib.pyplot as plt # 数据可视化

import numpy as np # 数值计算

import pandas as pd # 数据处理

salary_df = pd.read_csv("./Salary_dataset.csv") # 使用pd.read_csv更规范的写法

# 获取数据集维度信息

num_samples, num_features = salary_df.shape

print(f"样本数量: {num_samples}, 特征数量: {num_features}") # 使用f-string格式化

# 提取特征和标签(直接使用DataFrame列访问更高效)

years_exp = salary_df['YearsExperience'].tolist() # 工作经验作为特征

salary = salary_df['Salary'].tolist() # 薪资作为标签

# 创建画布和坐标系

fig = plt.figure(figsize=(10, 6)) # 设置画布尺寸

ax = fig.add_subplot(111) # 创建子图

# 设置坐标系参数

ax.set(

xlim=[0, 20], # X轴范围(工作年限)

ylim=[0, 150000], # Y轴范围(薪资)

title='Salary vs Experience', # 图表标题

xlabel='Years of Experience', # X轴标签

ylabel='Annual Salary (USD)' # Y轴标签

)

# 绘制散点图

ax.scatter(

years_exp,

salary,

color='red',

marker='+',

s=100, # 标记大小

label='Raw Data' # 图例标签

)

# 添加网格线

ax.grid(True, linestyle='--', alpha=0.7)

# 显示图表

plt.legend()

plt.tight_layout() # 自动调整布局

plt.show()

于该数据建立一元线性回归模型

y

=

w

1

+

x

y = w_1 + x

y=w1+x

我们可以等价与

h

θ

(

x

)

=

θ

0

+

θ

1

h_θ(x) = θ_0 + θ_1

hθ(x)=θ0+θ1

代价函数

均方误差(MSE)的代价函数为:

J

(

θ

0

,

θ

1

)

=

1

2

m

∑

i

=

1

m

(

h

θ

(

x

(

i

)

)

−

y

(

i

)

)

2

J( heta_0, heta_1) = frac{1}{2m} sum_{i=1}^{m} (h_ heta(x^{(i)}) - y^{(i)})^2

J(θ0,θ1)=2m1i=1∑m(hθ(x(i))−y(i))2

补充:这里采用 1 / 2 是为了梯度下降的时候简化计算

偏导数

对于

θ

0

和

θ

1

求偏导

对于 θ_0 和 θ_1求偏导

对于θ0和θ1求偏导

对

θ

0

:

对 θ_0:

对θ0:

∂

J

∂

θ

0

=

1

m

∑

i

=

1

m

(

h

θ

(

x

(

i

)

)

−

y

(

i

)

)

frac{partial J}{partial heta_0} = frac{1}{m} sum_{i=1}^{m} (h_ heta(x^{(i)}) - y^{(i)})

∂θ0∂J=m1i=1∑m(hθ(x(i))−y(i))

对

θ

1

:

对 θ_1:

对θ1:

∂

J

∂

θ

1

=

1

m

∑

i

=

1

m

(

h

θ

(

x

(

i

)

)

−

y

(

i

)

)

x

(

i

)

frac{partial J}{partial heta_1} = frac{1}{m} sum_{i=1}^{m} (h_ heta(x^{(i)}) - y^{(i)})x^{(i)}

∂θ1∂J=m1i=1∑m(hθ(x(i))−y(i))x(i)

对应代码 :

theta0

def compute_gradient_theta0(x: np.ndarray, y: np.ndarray,

theta0: float, theta1: float) -> float:

"""计算代价函数关于theta0的偏导数

Args:

x: 特征向量(工作年限)

y: 目标向量(薪资)

theta0: 当前截距参数

theta1: 当前斜率参数

Returns:

float: theta0的梯度值

"""

m = len(x)

hypothesis = theta0 + theta1 * x

return np.sum(hypothesis - y) / m # 向量化计算

theta1

def compute_gradient_theta1(x: np.ndarray, y: np.ndarray,

theta0: float, theta1: float) -> float:

"""计算代价函数关于theta1的偏导数"""

m = len(x)

hypothesis = theta0 + theta1 * x

return np.sum((hypothesis - y) * x) / m # 向量化计算

代价函数

def compute_cost(x: np.ndarray, y: np.ndarray,

theta0: float, theta1: float) -> float:

"""计算均方误差代价函数"""

m = len(x)

hypothesis = theta0 + theta1 * x

return np.sum((hypothesis - y) ** 2) / (2 * m)

梯度下降

def gradient_descent(x: np.ndarray, y: np.ndarray,

alpha: float, iterations: int) -> tuple:

"""执行梯度下降算法

Args:

alpha: 学习率

iterations: 迭代次数

Returns:

tuple: (最优theta0, 最优theta1)

"""

theta0, theta1 = 0.0, 0.0

cost_history = [] # 记录代价变化

for i in range(1, iterations + 1):

grad0 = compute_gradient_theta0(x, y, theta0, theta1)

grad1 = compute_gradient_theta1(x, y, theta0, theta1)

theta0 -= alpha * grad0

theta1 -= alpha * grad1

# 每1000次记录代价(可选)

if i % 1000 == 0:

cost = compute_cost(x, y, theta0, theta1)

cost_history.append(cost)

return theta0, theta1

全部代码

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd # 使用标准别名

# --------------------------

# 核心算法函数

# --------------------------

def compute_gradient_theta0(x: np.ndarray, y: np.ndarray,

theta0: float, theta1: float) -> float:

"""计算代价函数关于theta0的偏导数

Args:

x: 特征向量(工作年限)

y: 目标向量(薪资)

theta0: 当前截距参数

theta1: 当前斜率参数

Returns:

float: theta0的梯度值

"""

m = len(x)

hypothesis = theta0 + theta1 * x

return np.sum(hypothesis - y) / m # 向量化计算

def compute_gradient_theta1(x: np.ndarray, y: np.ndarray,

theta0: float, theta1: float) -> float:

"""计算代价函数关于theta1的偏导数"""

m = len(x)

hypothesis = theta0 + theta1 * x

return np.sum((hypothesis - y) * x) / m # 向量化计算

def compute_cost(x: np.ndarray, y: np.ndarray,

theta0: float, theta1: float) -> float:

"""计算均方误差代价函数"""

m = len(x)

hypothesis = theta0 + theta1 * x

return np.sum((hypothesis - y) ** 2) / (2 * m)

def gradient_descent(x: np.ndarray, y: np.ndarray,

alpha: float, iterations: int) -> tuple:

"""执行梯度下降算法

Args:

alpha: 学习率

iterations: 迭代次数

Returns:

tuple: (最优theta0, 最优theta1)

"""

theta0, theta1 = 0.0, 0.0

cost_history = [] # 记录代价变化

for i in range(1, iterations + 1):

grad0 = compute_gradient_theta0(x, y, theta0, theta1)

grad1 = compute_gradient_theta1(x, y, theta0, theta1)

theta0 -= alpha * grad0

theta1 -= alpha * grad1

# 每1000次记录代价(可选)

if i % 1000 == 0:

cost = compute_cost(x, y, theta0, theta1)

cost_history.append(cost)

return theta0, theta1

# --------------------------

# 主程序

# --------------------------

def main():

# 数据准备

data = pd.read_csv('./Salary_dataset.csv')

x = data['YearsExperience'].values # 转换为numpy数组

y = data['Salary'].values

# 超参数设置

alpha = 0.01 # 学习率

n = 5000

# 执行梯度下降

theta0, theta1 = gradient_descent(x, y, alpha, n)

# 结果输出

final_cost = compute_cost(x, y, theta0, theta1)

print(f"经过 {n} 次迭代:")

print(f"最终代价值: {final_cost:.2f}")

print(f"最优参数:theta0 = {theta0:.2f}, theta1 = {theta1:.2f}")

# 预测示例

# 注意:20年经验超出数据集范围,预测结果可能不可靠

experience_years = [4, 20]

for years in experience_years:

prediction = theta0 + theta1 * years

print(f"预测 {years} 年工作经验薪资: ${prediction:,.2f}")

# 可视化

plt.figure(figsize=(10, 6))

plt.scatter(x, y, color='red', marker='x', label='raw data')

# 生成回归线(扩展到数据范围外)

x_vals = np.linspace(0, x.max() + 5, 100)

y_vals = theta0 + theta1 * x_vals

plt.plot(x_vals, y_vals, 'b-', label='linear regression')

plt.title('years-salary', fontsize=14)

plt.xlabel('years', fontsize=12)

plt.ylabel('salary', fontsize=12)

plt.legend()

plt.grid(linestyle='--', alpha=0.7)

plt.tight_layout()

plt.show()

if __name__ == '__main__':

main()

站长推荐

- U8W/U8W-Mini使用与常见问题解决

U8W/U8W-Mini使用与常见问题解决

U8W/U8W-Mini使用与常见问题解决 - QT多线程的5种用法,通过使用线程解决UI主界面的耗时操作代码,防止界面卡死。

QT多线程的5种用法,通过使用线程解决UI主界面的耗时操作代码,防止界面卡死。...

QT多线程的5种用法,通过使用线程解决UI主界面的耗时操作代码,防止界面卡死。... - stm32使用HAL库配置串口中断收发数据(保姆级教程)

stm32使用HAL库配置串口中断收发数据(保姆级教程)

stm32使用HAL库配置串口中断收发数据(保姆级教程) - 分享几个国内免费的ChatGPT镜像网址(亲测有效)

分享几个国内免费的ChatGPT镜像网址(亲测有效)

分享几个国内免费的ChatGPT镜像网址(亲测有效) - SpringSecurity实现前后端分离认证授权

SpringSecurity实现前后端分离认证授权

SpringSecurity实现前后端分离认证授权