您现在的位置是:首页 >技术交流 >tsm9_Momentum_Ultimate Oscillators_MACDivergence index_Stochastic RSI_A/D Oscillator_RVI Vigor ADX网站首页技术交流

tsm9_Momentum_Ultimate Oscillators_MACDivergence index_Stochastic RSI_A/D Oscillator_RVI Vigor ADX

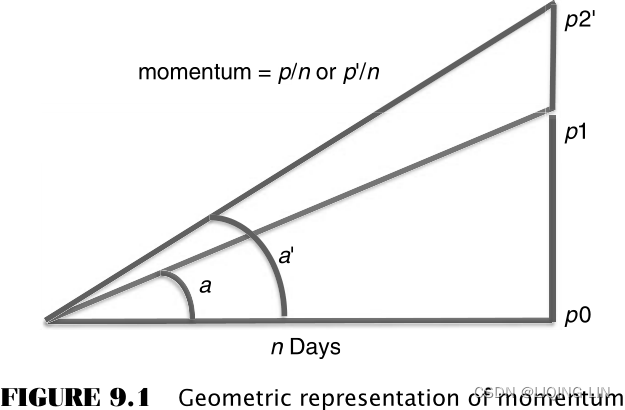

The study of momentum and oscillators is the analysis of price changes rather than price levels. Among technicians, momentum establishes the speed of price movement and the rate of ascent or descent.动量决定了价格变动的速度和上升或下降的速度 Analysts use momentum interchangeably with slope, the angle of inclination of price movement 斜率是价格变动的倾斜角度usually found with a simple least squares regression (Figure 9.1 a pure momentum oscillator that measures the percent change in price from one period to the next). In mathematics it is also the first difference, the difference between today’s price and the previous day. Momentum is often considered using terms of Newton’s Law, which can be restated loosely as once started, prices tend to remain in motion in more-or-less the same direction.

a pure momentum oscillator that measures the percent change in price from one period to the next). In mathematics it is also the first difference, the difference between today’s price and the previous day. Momentum is often considered using terms of Newton’s Law, which can be restated loosely as once started, prices tend to remain in motion in more-or-less the same direction.

Indicators of change, such as momentum and oscillators, are used as leading indicators of price direction. They can identify when the current trend is no longer maintaining its same level of strength; that is, they show when an upwards move is decelerating. Prices are rising, but at a slower rate. This gives traders an opportunity to begin liquidating their open trend trades before prices actually reverse. As the time period for the momentum calculation shortens, this indicator becomes more sensitive to small changes in price. It is often used in countertrend, or mean reversion strategy. The change in momentum, also called rate of change, acceleration, or second difference, is even more sensitive and anticipates change sooner.

Before beginning a discussion of various momentum calculations, a brief comment on terminology is necessary to understand how various techniques are grouped together. The use of a single price, such as Microsoft at $25.50 or gold at $1400, has no direction or movement implied. We are simply relating a price level and not indicating that prices are going up or down.

Next, we describe the speed at which prices are rising or falling. To know the speed, it is not enough to say that the S&P rose 3 points; you must specify the time interval over which this happened—“the S&P rose 3 points in 1 hour.” When you say that you drove your car at 60, you really imply that you were going 60 miles per hour, or 60 kilometers per hour. This description of speed, or distance covered over time, is the same information that is given by a single momentum value. Then, if the daily momentum of the NASDAQ 100 is +10, it is rising at the rate of 10 points per day.

Having made a point of saying that momentum is change over time, which it is, the “industry” uses momentum to mean price change with the time implied (and often not even given) where speed is always the price change divided by the time interval. The same interpretation will be used here. The term rate of change (ROC) will also be used to describe acceleration, an increase or decrease in the speed; when the rate of change is zero, we are talking about speed and momentum(Be careful about terminology. Many books and software use rate of change (ROC) interchangeably with momentum, the change in price over n days, rather than the change in momentum. Also, momentum indicators can also be used for mean reversion and may be called oscillators because their values swing from positive to negative.).

You will see in this chapter that acceleration is more sensitive than speed. We will begin with the least sensitive indicator, momentum, increase to acceleration, and then address the variations and applications, including divergence, the most popular use of momentum indicators.

MOMENTUM

Momentum is the difference between two prices taken over a fixed interval. It is an other word for speed, the distance covered over time; however, everyone uses it to mean change. For example, today’s 5-day momentum value would be the difference between M today’s price

is the difference between two prices taken over a fixed interval. It is an other word for speed, the distance covered over time; however, everyone uses it to mean change. For example, today’s 5-day momentum value would be the difference between M today’s price and the price five days ago:

- 5-day momentum,

- Using notation familiar to many programmers: 5-day momentum = price − price[5]

- or n-day momentum = price − price[n]

- where the notation [n] refers to the price n days ago.

The momentum value increases

as the change in price

increases over the same 5-day period. Figure 9.1

shows how the momentum changes as the price increases

over the same time period.

- Over n days, the price moves from

to

. It forms angle a and has a momentum of

.

For example, if the 5-day change in priceis an increase of 100, then the momentum is simply 100, but the speed is 100/5 = 20.

- If prices had increased to point

If prices increase by 100 points - When calculating momentum, the interval of the calculation must always be stated. To avoid confusion, we state that the 5-day momentum is 20 and the 10-day momentum is 10.

Today’s 5-day momentum, which we will now show as can range in value from the maximum upwards move

to the maximum downwards move

that the price can make in five days; the momentum is zero if prices are unchanged after five days. For stocks, there is no actual limit on the maximum price range over any time interval. In cases such as Enron, prices could collapse to zero in short order. From a practical view, most stocks and futures markets have a history of volatility that relates to their price level. The higher the price, the greater the price moves. As the price of gold rose to $1000 per ounce, the 5-day momentum could have been as high as $100 per ounce ($20 per day). When it was at $250 and investors lost interest, it may have shown a $1 per ounce change over five days.

Momentum is not volatility. Gold can move from $1200 to $1250 in two days then back to $1200 over the next three days and the momentum would be zero but the volatility would be high.

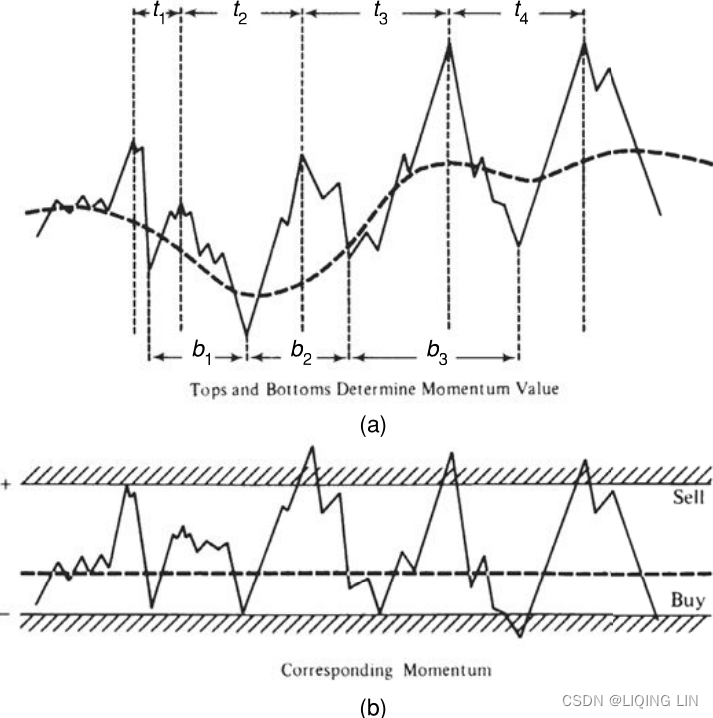

Figure 9.2 shows a typical pattern of momentum. Smooth prices are used to make the relationship between price change and momentum clear.

Figure 9.2 shows a typical pattern of momentum. Smooth prices are used to make the relationship between price change and momentum clear.

- During the first 15-day cycle, prices rise steadily, peaking on day 9.

- As prices rise at a slower rate during days 5 through 9 the momentum declines but remains above zero.

As long as the 5-day momentum is greater than zero, prices are rising. - The highest momentum

value occurs on day 3 when prices have the largest positive price change.

- On day 10 the momentum value is zero. Looking at the price chart, this occurs when the 5-day change in price is zero.

- The lowest momentum value occurs on day 16 when the prices have declined the most.

- After prices reach their lowest point and begin up, the momentum is negative but rising.

If prices always moved in the smooth pattern shown in Figure 9.2, then momentum would be a perfect leading indicator. You could buy when momentum turned up and sell when it turned down, and be ahead of the change in price direction. Unfortunately, prices movement is irregular; consequently, momentum values are irregular. Because momentum contains valuable information, we will look at a number of systematic ways to evaluate momentum and improve trading. These focus on extreme momentum values and momentum patterns, all of which have proved to be valuable additions to trading strategies, in particular to the timing of entries and exits.

Characteristics of Momentum

Momentum is a way of smoothing price movement and can serve the same purpose as a trend. Although the momentum values are not as smooth as a moving average, larger momentum periods reduce the extremes seen in the price chart. One key advantage of momentum is that it does not have the lag that exists in a moving average.

The AOL chart (Figure 9.3) compares 20- and 40-day moving averages at the top with 20- and 40-day momentum along the bottom. The 40-day momentum (dark line) is smoother and peaks at about the same place as the price. The faster 20-day momentum is not as smooth but peaks sooner than the 40-day momentum and actually leads the price movement. The peaks of the faster momentum represent the maximum price change over a 20-day period. Had prices continued higher at the same rate—that is, if prices had increased $1 per day—the 20-day momentum would have turned sideways and become a horizontal line.

The 20-day and 40-day momentum lines both peak significantly sooner than their moving average equivalents, showing that the speed represented by momentum is a more sensitive measure than the direction of a trendline. The cost of this leading indicator is the increased noise seen in the erratic pattern of momentum compared to the smoothness of the trendline.

Momentum can be used as a trend indicator by

- selling when the momentum value crosses downward through the horizontal line at zero

- and buying when it crosses above the zero line.

Because there is more noise in momentum than in the equivalent moving average, you would want to draw a small band around the zero line about the width of the small variations in momentum.

- A sell signal would be given when the momentum falls below the lower band and

- a buy when it moves upward through the upper band.

However, the momentum crossing zero is essentially the same as the moving average turning up or down. It means that the price today is the same as the price n-days ago. Chapter 8 compared the performance of a trend and a momentum system over the same calculation periods.

Momentum as a Percentage

It is always convenient to express all markets in the same notation. It makes comparisons much easier. For the stock market, momentum can be expressed as a percentage where a 1-day momentum is equivalent to the 1-day return,or, because they are returns, the alternative can be used, ln

. But momentum is most often calculated over more than one day; therefore, the n-day momentum as a percentage is

Using percentages does not work for futures markets because most data used for analysis are continuous, back-adjusted prices. Back-adjusting over many years and many contracts will cause the oldest data to be very different from the actual prices that occurred on those dates; therefore, percentages are incorrect. When using momentum with back-adjusted futures prices, it is best to use the price differences.

Momentum as the Difference between Price and Trend

The term momentum is very flexible. It is common for it to refer to the difference between today’s price and a corresponding moving average value, in a manner similar to beta, which indicates the relative strength of a stock compared to an index. The properties of this new value are the same as standard momentum.动量一词非常灵活。 它通常指的是今天的价格与相应的移动平均值之间的差异,其方式类似于 beta,表示股票与指数相比的相对强度。 这个新值的属性与标准动量相同

- As the momentum becomes larger, prices are moving away from the moving average.

- As it moves towards zero, the prices are converging with the moving average.

FIGURE 9.4 Momentum is also called relative strength, the difference between two prices or a price and a moving average (lower panel). The traditional momentum calculation is shown in the center panel.

FIGURE 9.4 Momentum is also called relative strength, the difference between two prices or a price and a moving average (lower panel). The traditional momentum calculation is shown in the center panel.

The upper panel of Figure 9.4 shows a 20-period moving average plotted on a daily chart of Intel during the 14 months ending May 2003.

- The center panel shows the standard 20-period momentum, the difference between prices that are 20 days apart.

- The range of values for the center panel is approximately +6 to −11

- The bottom panel is the difference between the price and the 20-day moving average.

- the scale on the lower panel is +3 to −7.

- Because a trendline lags behind price movement, the difference between the price and trendline is smaller at points where there are larger price swings 价格波动较大and typically larger momentum values(compare to the smallest negative momentum) 动量值通常较大.

A comparison of the two lower panels of Figure 9.4 also shows that there are differences in the small movements but the overall pattern is the same. When a price moves to an extreme, it is generally farthest from the moving average and farthest from the price n-days ago; therefore, the most extreme points occur at exactly the same place. This momentum calculation has also been called relative strength because it is measured relative to a previous price or relative to a trendline.

Momentum as a Trend Indicator

The momentum value is a smoothing of price changes and can serve the same purpose as a standard moving average. Many applications use momentum as a substitute for a price trend. By looking at the net change in price over the number of days designated by an n-day momentum indicator, intermediate fluctuations are ignored, and the pattern in price trend can be seen. The longer the span between the observed points, the momentum calculation period, the smoother the results. This is very similar to faster and slower moving averages.

In its simplest form, momentum is simply the difference between the current price and price of some fixed time periods in the past.

- Consecutive periods of positive momentum values indicate an uptrend;

- conversely, if momentum is consecutively negative, that indicates a downtrend.pa8_Contract for Difference CFD Trading_Oanda_git_log return_Momentum Strategy_Leverage_margin_tpqoa_LIQING LIN的博客-CSDN博客

To use momentum as a trend indicator, choose any calculation period.

- A buy signal occurs whenever the value of the momentum turns from negative to positive, and

- a sell signal is when the opposite occurs, as shown in Figure 9.5.

FIGURE 9.5 Trend signals using momentum.

FIGURE 9.5 Trend signals using momentum. - If a band is used to establish a neutral position or a commitment zone如果使用带来建立中性位置或保证(承诺)区, as discussed in the previous chapter, it should be drawn around the horizontal line representing the zero momentum value.

In order to find the best choice of a momentum span, a sampling of different values could be tested for optimum performance, or a chart could be examined for some natural price cycle.

- Identify the significant tops and bottoms of any bar chart, and average the number of days between these cycles,

- or find the number of days that would closely approximate the occurrences of these peaks and valleys. Then use ½ or ¼ the number of days from peak to peak or valley to valley. These natural cycles will often be the best choice of momentum calculation interval (Figure 9.6).

FIGURE 9.6 Relationship of momentum to prices. (a) Tops and bottoms determine momentum value. (b) Corresponding momentum.

FIGURE 9.6 Relationship of momentum to prices. (a) Tops and bottoms determine momentum value. (b) Corresponding momentum. - Momentum and oscillators, however, are more often used to identify abnormal price movements and for timing of entries and exits in conjunction with a longer-term trend. 动量和震荡指标更常用于识别异常价格变动以及结合长期趋势确定进入和退出的时机。

Timing an Entry确定进入的时机

Momentum is a convenient way of identifying good entry points based on small price reversals within a trend that are not large enough to change the direction of the trend. By choosing a much shorter time period for the momentum calculation (for example, 6 days) to work in combination with a longer trend of 30 to 50 days, the momentum indicator will show frequent opportunities within the trend. The short time period for the momentum calculation assures you that there will be an entry opportunity within about 3 days of the entry signal; therefore, it becomes a practical timing tool. This is particularly useful when you view momentum as a countertrend signal, which will be discussed in the next section. Examples of using a momentum as entry timing can also be found in Chapter 19.

Identifying and Fading Price Extremes识别和消退价格极端

An equally popular and more interesting use for momentum focuses on the analysis of relative tops and bottoms. All momentum values are bounded (although somewhat irregularly) in both directions by the maximum move possible during the time interval represented by the span of the momentum. The conditions at the points of high positive and negative momentum are called overbought and oversold, respectively.

A market is

- overbough when it can no longer sustain the strength of the current uptwards trend and a downward price reaction is imminent / ˈɪmɪnənt /即将发生的,临近的;

- an oversold market is ready for an upward move.

- Faster momentum calculations (those using shorter calculation periods) will tend to fluctuate above and below the zero line based on small price changes.

- Longer calculation periods will take on the characteristics of a trend and stay above or below the zero line for the extent of the trend.较长的计算周期将呈现趋势特征,并在趋势范围内保持在零线上方或下方

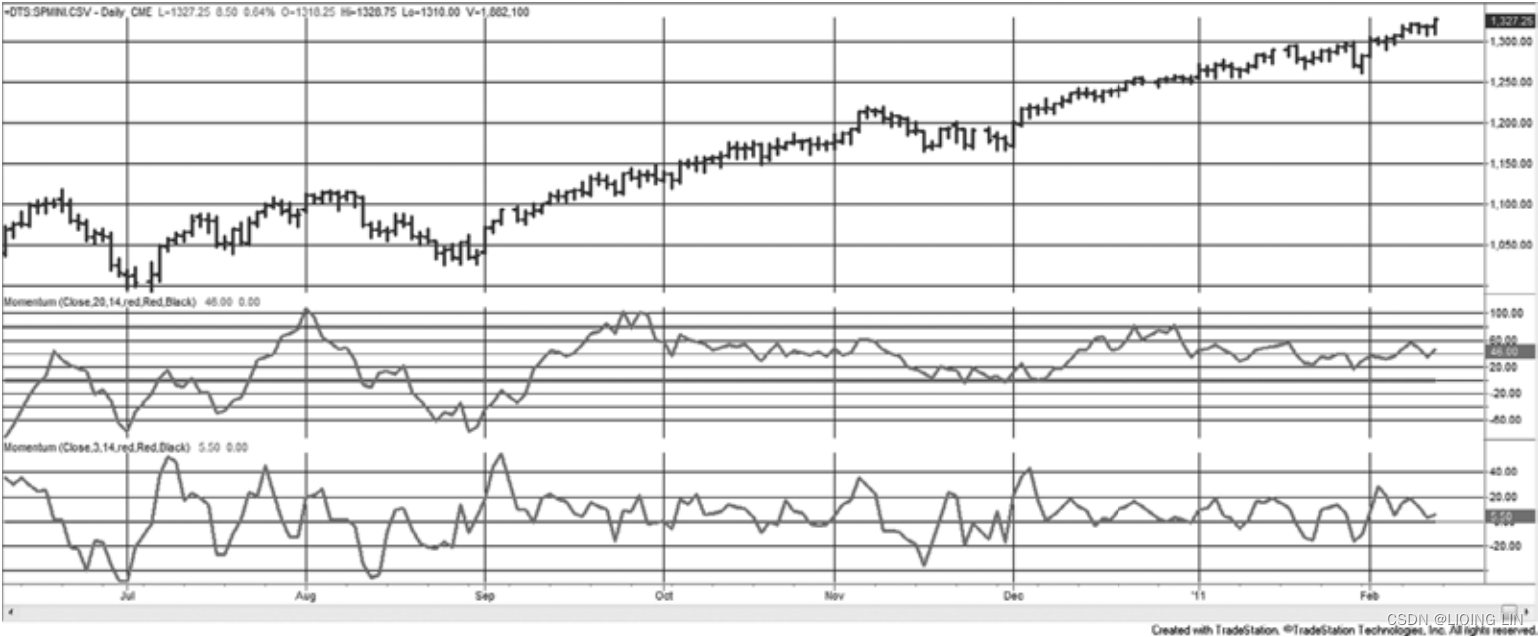

In Figure 9.7, using S&P futures,

- the 20-day momentum in the center panel stays above zero for most of the period from September 2010 through February 2011.

- The very fast 3-day momentum in the bottom panel consistently penetrates the zero line, although the peaks on the upside are larger than those on the downside.

FIGURE 9.7 20-day momentum (center panel) and 3-day momentum (bottom panel) applied to

FIGURE 9.7 20-day momentum (center panel) and 3-day momentum (bottom panel) applied to

the S&P, June 2010 through February 2011.

The values on the right scale of the two lower panels in Figure 9.7 show the range of price movement over the 20-day and 3-day periods. The 20-day scale goes from +100 to –60 while the 3-day scale is smaller, about +60 to –40. The 3-day momentum is not 3/20ths of the 20-day momentum(3 天动量不是 20 天动量的 3/20) because volatility does not increase linearly over time. That is, volatility can increase faster in a few days, but over longer periods it has up and down movement that limits the total move in one direction. 波动率在几天内可能会增加得更快,但在更长的时间里,它会上下波动,从而限制一个方向的总波动。

A system can take advantage of the momentum extremes by fading the price movement (selling rallies and buying declines逢高卖出和下跌买入). This is done by drawing two horizontal lines on the momentum chart (as shown in Figure 9.6b) above and below the zero line in such a way that the tops and bottoms of the major moves are isolated. These lines may be selected

- • Visually, so that once the line is penetrated/ ˈpenətreɪtɪd /穿透, prices reverse shortly afterwards.

- • Based on a percentage of the maximum possible momentum value.

- • A multiple of the standard deviation of momentum values. Using two standard deviations would position the lines so that only 5% of all momentum values penetrate above and below the two horizontal lines

When positioning these bands, there is always a trade-off between finding more trading opportunities and entering the market too soon. This can be a complicated choice and is discussed in “System Trade-Offs” in Chapter 22. Once these lines have been drawn, the entry options will be one of the following basic trading rules:

- • Aggressive.

- Enter a new long position when the momentum value penetrates the lower bound;

- enter a new short position when the value penetrates the upper bound.

- • Minor confirmation.

- Enter a new short position on the first day the momentum value turns down after penetrating the upper bound

- (the opposite for longs).

- Enter a new short position on the first day the momentum value turns down after penetrating the upper bound

- • Major confirmation.

- Enter a new short position when the momentum value penetrates the upper bound moving lower

- (the opposite for longs).

- • Timing.

- Enter a new short position after the momentum value has remained above the upper bound for n days

- (the opposite for longs).

To close out a profitable平仓获利的 short or long position, there are the following alternatives (the rules are symmetrical for longs and shorts):

- • Most demanding.

- Close out long positions or cover shorts when the momentum value satisfies the entry condition for a reverse position.当动量值满足反向头寸的入场条件时,平掉多头头寸或回补空头头寸。

- • Moderately demanding.

- Cover a short position when the momentum penetrates the 0 line, minus one standard deviation (or some other target point partway between the zero line and the lower bound).当动量穿透零线,减去一个标准偏差(或零线和下限之间的某个其他目标点)时平仓。

- • Basic exit. Cover a short position when the momentum value becomes 0.

- • Allowing an extended move.

- Cover a short position if the momentum crosses the 0 line moving up after penetrating that line moving down.

The basic exit, removing your trade when the momentum reaches the 0 line, is the benchmark case. It is based on the conservative/kənˈsɜːrvətɪv/保守的 assumption that prices will return to the center of the recent movement (in other words, mean reverting). It is less reasonable to assume that prices will continually move from overbought to oversold and back again. Most statisticians would agree that the mean is the best forecast of future prices, and the 0 momentum value represents the mean. You may try to increase the profits by assuming that the momentum value will penetrate the zero line by a small amount 您可以通过假设动量值会少量穿过零线来尝试增加利润 because there is always some amount of noise. However, if you require a larger penetration of zero to cause an exit, many of the exit opportunities will be lost如果您需要更大的零渗透来导致退出,那么许多退出机会将会丢失 You can be more conservative by exiting somewhat before the zero line is reached, but then you also reduce your average profit.您可以通过在达到零线之前稍微退出来更加保守,但这样您也会降低平均利润。

The same momentum calculations, viewed over a longer time period, show one of the problems with using momentum for timing. Figure 9.8 covers a critical period, from August 2005 through February 2011. Notice that the scale of the momentum values change dramatically from the beginning to the end of the chart.

- This is especially important for the 20-day momentum in the middle panel. For all of 2006, volatility was very low. Had we used momentum as an overbought/oversold indicator, the entry bands would have been at about ±30.

- For the 3-day momentum, it would have been closer to ±15.

- As we saw before, the faster momentum is more symmetric than the slower one. During 2006, there were more selling than buying opportunities(注意 : 多个向下穿过水平线).

FIGURE 9.8 A longer view of the 20- and 3-day momentum applied to the S&P. The magnitude

FIGURE 9.8 A longer view of the 20- and 3-day momentum applied to the S&P. The magnitude

of the momentum values change over time.

Volatility increases in 2007. If buy entries were targeted as momentum values of −30 then traders would have held a 120 point loss as momentum dropped to −150. A similar pattern was repeated on the upside for sell signals. It would be necessary to increase the width of the buy and sell bands to ±75 and still hold larger losses waiting for a price reversal. But then comes 2008, and any countertrend entry, buying as prices fall, would have caused a complete loss of equity. However, let’s say that we were able to avoid disaster and the entry-exit bands were at ±100 for the 20-day momentum and ±50 for the 3-day. Volatility finally declines and we get only the occasional entry signal. The bands need to be adjusted back down to a smaller range.

The problem with using momentum for timing is that the scale is unpredictable. Even if we waited for a reversal after penetrating the band there is no assurance that prices will not reverse and go to new extremes. Some risk protection is needed, a way of dynamically adjusting the bands (as discussed in Chapter 8), or a different way of measuring momentum.

Risk Protection

A protective stop-loss order can be used whenever you trade against the current price momentum. A stop-loss is a specific order to exit if the price goes the wrong way (discussed in Chapter 23 but also throughout the book). This is most important with the aggressive entry激进的入场, which advocates selling when the momentum value moves above the upper threshold line, regardless of how fast prices are rising. While the other entry options allow for a logic positioning of a stop-loss其他入场选项允许止损的逻辑定位, the aggressive entry does not. You will simply need to decide, based on historic momentum values, where to limit your risk 您只需要根据历史动量值来决定在何处限制您的风险. With the other entry options, prices are no longer at their extremes于其他入场选项,价格不再处于极端, so that stops may be placed using one of the following techniques:

- • Place a protective stop above or below the most extreme high or low momentum value.在最高或最低动量值上方或下方设置保护性止损

- • Follow a profitable move with a trailing, nonretreating stop based on fixed points or a percentage.遵循基于固定点或百分比的追踪、非撤退止损的获利走势。

- • Establish zones that act as levels of attainment (using horizontal lines of equal spacing), and do not permit reverse penetrations once a new zone is entered.建立作为达到水平的区域(使用等间距的水平线),并且一旦进入新区域就不允许反向渗透

Risk protection must be flexible in the way it deals with volatility. As prices reach higher levels, increased volatility will cause momentum tops and bottoms to widen; with low volatility, prices may not be active enough to penetrate the upper or lower bounds.随着价格达到更高水平,波动性增加将导致动量顶部和底部扩大; 在低波动率的情况下,价格可能不够活跃,无法突破上限或下限。 This is shown in Figure 9.8. Therefore, both the profits and risk of a trade entered at extremes must increase with volatility and higher prices. Stops could be based on a percentage of price or a multiple of volatility进入极端交易的利润和风险都必须随着波动性和更高的价格而增加。 止损可以基于价格的百分比或波动率的倍数。.

The aggressive entry option remains the greatest problem for controlling risk, where a short signal is given when prices are very strong. If an immediate reversal does not occur, large open losses may accrue. To determine the proper stop-loss amount, a computer test was performed using an immediate entry based on penetration of an extreme boundary and with a stop-loss at the close of the day for risk protection. The first results were thought to have outstanding profits and consistency until it was discovered that the computer had done exactly the opposite of what was intended—it bought when the momentum crossed the upper bound and placed a close stop-loss below the entry. It did prove, for a good sampling of futures markets, that high momentum periods continued for enough time to capture small but consistent profi ts. It also showed that the aggressive entry trading rule, anticipating an early reversal, would be a losing strategy. One should never forget that declining momentum does not mean that prices are falling.激进的进场选择仍然是控制风险的最大问题,当价格非常强劲时会发出空头信号。 如果没有立即发生逆转,则可能会累积大量未平仓损失。 为了确定适当的止损金额,我们使用基于突破极端边界的即时入场和在当日收盘时设置止损以保护风险进行了计算机测试。 最初的结果被认为具有出色的利润和一致性,直到发现计算机所做的与预期的完全相反——它在动量越过上限时买入,并在入口下方设置了止损。 它确实证明,对于一个很好的期货市场样本,高动能期持续了足够长的时间来获取小而稳定的利润。 它还表明,预期早期逆转的进取交易规则将是一种失败的策略。 人们永远不应忘记,势头下降并不意味着价格正在下跌。

The Trend Provides Protection

In these examples, momentum is not a strategy itself, but a way of entering a trend trade. When a trend signal first occurs, it is not entered. If the signal was long, then the strategy waits until the 3-day momentum penetrates the lower band. If prices continue lower, then the trend will change from up to down, and the position will be exited. It would not be necessary to have a stop-loss.

Profit Targets for Fading Extreme Moves消退极端走势的利润目标

When using momentum as a mean-reversion strategy, the most reasonable exit for a short entered at an extreme momentum high, or a long position entered at a low, is when the momentum returns to near zero. Prices do not have an obligation to go from extreme lows to extreme highs; however, any extreme can be expected to return to normal, which is where momentum is zero. Returning to zero does not mean that all trades will be profitable. If there has been a strong upwards move that lasted longer than the calculation period of the momentum, then prices will be higher when momentum finally returns to zero. The trend is not your friend if it fights with your mean-reversion position.

The number of profitable trades can be increased by targeting a momentum level that is more conservative than zero. That is, if a long was entered at an extreme low, a sell would be placed 5% or 10% below the zero momentum line, based on the distance between the buying threshold line and zero. Trades that almost return to normal would then be closed out with profits, although the average size of the profi t would be smaller. To increase the size of the profits per trade, you would target the opposite side of the zero momentum line; therefore, if you held a long position, you would wait until the momentum value was greater than zero by 5% or 10% of the range. The success of taking profits early or late depends on the amount of noise in the momentum values as it fluctuates near the zero value. In many cases where extreme prices are followed by a sideways pattern, momentum will fluctuate around zero so that there is ample opportunity to exit the trade at a better price.在许多情况下,极端价格之后是横向形态,动量将在零附近波动,因此有足够的机会以更好的价格退出交易。

High-Momentum Trading

Some professional traders have made a business of trading in the direction of the price move only when momentum exceeds the high threshold level rather than anticipating a change of direction. There is a small window of opportunity when prices are moving fast. They will usually continue at the same, or greater, momentum for a short time, measured usually in minutes or hours, but occasionally a few days. There is a lot of money to be made in a short time—but at great risk if prices reverse direction sooner than expected.

Price patterns have changed. There are many more day traders. When one stock breaks out above a previous high, everyone sees it as an opportunity for profit. Buy orders start to flow, and volume increases. Stocks that are normally ignored can attract large volume when prices make a new high. Traders ride the rising prices for as long as possible, watching to see when volume begins to drop, then they exit. Some may just target a modest profit and get out when that target is reached.

High-momentum trading is a fast game that requires tools that allow you to scan a wide range of stocks. You are looking for one that has made a new high after a long, quiet period寻找经过长期平静期后创下新高的股票. You may also continually sort stocks by the highest momentum values还可以根据最高动量值不断对股票进行排序. You need to stay glued to your screen, enter fast and exit fast您需要紧盯着屏幕,快速进入并快速退出. It is a full-time commitment.

(MACD Trend indicator)Moving Average Convergence/Divergence

Many of the practical problems of fading prices using momentum are solved with the Moving Average Convergence Divergence (MACD), developed by Gerald Appel. The MACD uses momentum calculated as the difference between two trendlines, produced using exponential smoothing. This momentum value is further smoothed to give a signal line. The most common form of MACD uses the difference between a 12-day and 26-day exponential smoothing. The signal line, used to produce trading recommendations, is a 9-day smoothing of the MACD. The MACD can be created as follows:

Many of the practical problems of fading prices using momentum are solved with the Moving Average Convergence Divergence (MACD), developed by Gerald Appel. The MACD uses momentum calculated as the difference between two trendlines, produced using exponential smoothing. This momentum value is further smoothed to give a signal line. The most common form of MACD uses the difference between a 12-day and 26-day exponential smoothing. The signal line, used to produce trading recommendations, is a 9-day smoothing of the MACD. The MACD can be created as follows:

- Step 1: Choose the two calculation periods for the trend,

- for example, 20 and 40.

- Convert to smoothing constants(smoothing factors) using 2/(n + 1).

- Step 2: Calculate the slow trendline, EMA40, using the smoothing value 0.0243

.

- Step 3: Calculate the fast trendline, EMA20, using the smoothing value 0.0476.

- Step 4: The MACD line, the slower-responding line in the bottom panel of Figure 9.9, is EMA20 – EMA40. When the market is moving up quickly, the fast smoothing will be above the slow, and the difference will be positive. This is done so that the MACD line goes up when prices go up.

- Step 5: The signal line is the 9-day smoothing (using a constant of 0.10) of the MACD line. The signal line is slower than the MACD; therefore, it can be seen in the bottom panel of Figure 9.9 as the lower line when prices are moving higher.t2_Deciphering the Market_ticklabels_sma_ewma_apo_macd_Bollinger_Momentum_statsmodels_adfuller_ARIMA_LIQING LIN的博客-CSDN博客

ema_fast = (close_price - ema_fast) * K_fast + ema_fastclose = goog_data['Close'] num_periods_fast = 20 # time period for the fast EMA K_fast = 2/(num_periods_fast+1) # smoothing factor for fast EMA ema_fast = 0 # initial ema num_periods_slow = 40 # time period for slow EMA K_slow = 2/(num_periods_slow+1) # smoothing factor for slow EMA ema_slow = 0 # initial ema num_periods_macd = 9 # MACD ema time period K_macd = 2/(num_periods_macd+1) # MACD EMA smoothing factor ema_macd= 0 ema_fast_values = [] # we will hold fast EMA values for visualization purposes ema_slow_values = [] # we will hold slow EMA values for visualization purposes macd_values = [] # tract MACD values for visualization purpose # MACD = EMA_fast - EMA_slow macd_signal_values = [] # MACD EMA values tracker # MACD_signal = EMA_MACD macd_histogram_values = [] # MACD = MACD - MACD_signal for close_price in close: if ema_fast == 0: # first observation ema_fast = close_price ema_slow = close_price else: ema_fast = (close_price - ema_fast) * K_fast + ema_fast ema_slow = (close_price - ema_slow) * K_slow + ema_slow ema_fast_values.append( ema_fast ) ema_slow_values.append( ema_slow ) macd = ema_fast - ema_slow # MACD is fast_MA - slow_EMA # apo_values if ema_macd == 0 : ema_macd = macd else: ema_macd = (macd-ema_macd) * K_macd + ema_macd # signal is EMA of MACD values macd_values.append( macd ) macd_signal_values.append( ema_macd ) macd_histogram_values.append( macd-ema_macd )

ema_slow = (close_price - ema_slow) * K_slow + ema_slow

adjust=False

adjust=True ==> Expanding out EMA_old...

等式的上方是对当前价格到最初价格的加权求和,用的加权因子是

等式的下方是对所有加权因子的求和(可用等比例求和公式)

等比例求和公式推导

and

and (公比

(公比 )

)

==>

==>

mpf11_3_status_plotly Align dual Yaxis_animation_button_MFI_Williams %Rsi_AO Co_VWAP_MAcd_BollingerB_LIQING LIN的博客-CSDN博客

def get_macd( df, MACD_EMA_SHORT=12, MACD_EMA_LONG=26, MACD_EMA_SIGNAL=9 ): """ Moving Average Convergence Divergence This function will initialize all following columns. MACD Line (macd): (12-day EMA - 26-day EMA) Signal Line (macds): 9-day EMA of MACD Line MACD Histogram (macdh): MACD Line - Signal Line :param df: data :return: None """ close = df['Close'] fast = close.ewm(ignore_na=False, span=MACD_EMA_SHORT,# span:window size ==> a=2/(span+1) : decay or smoothing factor min_periods=0, # Minimum number of observations in window required to have a value adjust=True # the EW function is calculated using weights ).mean() slow = close.ewm(ignore_na=False, span=MACD_EMA_LONG,# span:window size ==> a=2/(span+1) : decay or smoothing factor min_periods=0, # Minimum number of observations in window required to have a value adjust=True # the EW function is calculated using weights ).mean() df['macd'] = fast - slow # Signal Line (macds): 9-day EMA of MACD Line df['macds_{}'.format(MACD_EMA_SIGNAL)] = df['macd'].ewm(ignore_na=False, span=MACD_EMA_SIGNAL,# span:window size ==> a=2/(span+1) : decay or smoothing factor min_periods=0, # Minimum number of observations in window required to have a value adjust=True # the EW function is calculated using weights ).mean() df['macdh_{}_{}'.format(MACD_EMA_SHORT, MACD_EMA_LONG)] = (df['macd'] - df['macds_{}'.format(MACD_EMA_SIGNAL)]) # MACD Histogram (macdh): MACD Line - Signal Line return df

The 20- and 40-day momentum lines(NOTE The term momentum is very flexible. It is common for it to refer to the difference between today’s price and a corresponding moving average value: and

), corresponding to the MACD line and the histogram, are shown in the center panel of Figure 9.9.

FIGURE 9.9 MACD for AOL. The MACD line is the faster of the two trendlines in the bottom panel; the signal line is the slower. The histogram is created by subtracting the slower signal line

FIGURE 9.9 MACD for AOL. The MACD line is the faster of the two trendlines in the bottom panel; the signal line is the slower. The histogram is created by subtracting the slower signal line

from the MACD line.

It is clear that the MACD process smoothes these values significantly; therefore, it makes trading signals easier to see.

Trading the MACD

The most common use of the MACD is as a trend indicator. For this purpose, only the MACD and signal lines are used in the following way:

- Buy when the MACD line (faster) crosses upwards through the signal line (slower).

- Sell when the MACD line crosses from above to below the signal line.

In the bottom panel of Figure 9.9, the buy signals that occur right after an extreme low in April and October of 2001 generated large gains. Unfortunately, there were many other crossings that generated losses; therefore, it is necessary to select which trades to enter. To accomplish that, the MACD uses thresholds similar to those shown for momentum, but in the opposite way. The MACD must first penetrate the lower band; then it must signal a new uptrend before a long position can be entered. In this way, it removes some of the whipsaws that might occur in a sideways market. Threshold levels were established by observing the historically high and low momentum values, shown as horizontal lines at the +2.00 and −2.00 levels in Figure 9.9. Sell signals would have been taken only after the MACD value had been above +2.00, and buy signals only when the MACD value had fallen below −2.00. The trading signals that satisfy these conditions are the buy signal in April, a sell a in May, and a buy a in October. However, fitting the threshold lines make them unreliable values for trading但是,拟合阈值线会使它们成为不可靠的交易值. One solution can be found in “An RSI Version of MACD” in the next section.

Appel has written extensively on the MACD, and many variations can be found in his book, Technical Analysis( Gerald Appel, Technical Analysis, Power Tools for Active Investors (Upper Saddle River, NJ: FT Prentice Hall, 2005) ). Many of the examples are interpretive, similar to the way we look at chart patterns. Appel also preferred using trends of 19 and 39 days for the NASDAQ composite. An equally important use of MACD is for divergence signals. Bearish divergence occurs when prices are rising but the MACD values are falling. Because this technique applies to many indicators in addition to the MACD, it is covered in detail in the section “Momentum Divergence” toward the end of this chapter.

Interpretation

- The Moving Average Convergence/Divergence (MACD, or MAC-D) line is calculated by subtracting the 26-period exponential moving average (EMA) from the 12-period EMA. The signal line is a 9-period EMA of the MACD line.

- MACD is best used with daily periods, where the traditional settings of 26/12/9 days is the norm.

- MACD triggers technical signals when the MACD line crosses above the signal line (to buy) or falls below it (to sell).

- MACD can help gauge/ ɡeɪdʒ / whether a security is overbought or oversold, alerting traders to the strength of a directional move, and warning of a potential price reversal.

MACD 可以帮助衡量证券是超买还是超卖,提醒交易者定向移动的强度,并警告潜在的价格反转。 - MACD can also alert investors to bullish/bearish divergences (e.g., when a new high in price is not confirmed by a new high in MACD, and vice versa), suggesting a potential failure and reversal.

MACD 还可以提醒投资者注意看涨/看跌背离(例如,当 MACD 的新高未确认价格的新高时,反之亦然),表明潜在的失败和逆转。 - After a signal line crossover, it is recommended to wait for three or four days to confirm that it is not a false move.

信号线交叉后,建议等待三四天,确认不是假动作。

As its name implies, the MACD is all about the convergence and divergence of the two exponential moving averages. Convergence occurs when the moving averages move towards each other. Divergence occurs when the moving averages move away from each other. The shorter moving average (12-day) is faster and responsible for most MACD movements. The longer moving average (26-day) is slower and less reactive to price changes in the underlying security.

The MACD line oscillates above and below the zero line, which is also known as the centerline. These crossovers signal that the 12-day EMA has crossed the 26-day EMA. The direction, of course, depends on the direction of the moving average cross.

- Positive MACD indicates that the 12-day EMA is above the 26-day EMA. Positive values increase as the shorter EMA diverges further from the longer EMA. This means upside momentum is increasing.

- Negative MACD values indicate that the 12-day EMA is below the 26-day EMA. Negative values increase as the shorter EMA diverges further below the longer EMA. This means downside momentum is increasing.

In the example above,

In the example above,

- the yellow area shows the MACD line in negative territory as the 12-day EMA trades below the 26-day EMA. The initial cross occurred at the end of September (black arrow) and the MACD moved further into negative territory as the 12-day EMA diverged further from the 26-day EMA.

- The orange area highlights a period of positive MACD values, which is when the 12-day EMA was above the 26-day EMA.

Notice that the MACD line remained below 1 during this period (red dotted line). This means the distance between the 12-day EMA and 26-day EMA was less than 1 point, which is not a big difference. 请注意,MACD 线在此期间保持在 1 以下(红色虚线)。 这意味着 12 天 EMA 和 26 天 EMA 之间的距离小于 1 点,相差不大。

Signal Line Crossovers

信号线交叉是最常见的 MACD 信号。 信号线是 MACD 线的 9 天 EMA。 作为指标的移动平均线,它落后于 MACD 并且更容易发现 MACD 转向。

- 当 MACD 向上并穿过信号线时,出现bullish crossover。

- 当 MACD 向下并穿过信号线下方时,出现bearish crossover。

- 交叉可以持续几天或几周,具体取决于移动的强度。

当交叉符合流行趋势时,它们更可靠。 如果 MACD 在长期上升趋势中经过短暂的下行修正后上穿其信号线,则有资格确认看涨并可能延续上升趋势。

如果 MACD 在长期下降趋势中短暂走高后下穿信号线,交易员会认为这是看跌确认。

Due diligence尽职调查/ ˈdɪlɪdʒəns / is required before relying on these common signals. Signal line crossovers at positive or negative extremes should be viewed with caution. Even though the MACD does not have upper and lower limits, chartists can estimate historical extremes with a simple visual assessment. It takes a strong move in the underlying security to push momentum to an extreme. Even though the move may continue, momentum is likely to slow and this will usually produce a signal line crossover at the extremities. Volatility in the underlying security can also increase the number of crossovers.

MACD 通常以直方图(见下图)显示,该直方图描绘了 MACD 与其信号线之间的距离。 如果 MACD 高于信号线,则直方图将高于 MACD 的基线或零线。 如果 MACD 低于其信号线,则直方图将低于 MACD 的基线。 交易者使用 MACD 的柱状图来确定何时看涨或看跌势头高——以及可能超买/超卖。

The chart shows IBM with its 12-day EMA (green), 26-day EMA (red) and the 12,26,9 MACD in the indicator window. There were eight signal line crossovers in six months: four up and four down. There were some good signals and some bad signals. The yellow area highlights a period when the MACD line surged above 2 to reach a positive extreme. There were two bearish signal line crossovers

The chart shows IBM with its 12-day EMA (green), 26-day EMA (red) and the 12,26,9 MACD in the indicator window. There were eight signal line crossovers in six months: four up and four down. There were some good signals and some bad signals. The yellow area highlights a period when the MACD line surged above 2 to reach a positive extreme. There were two bearish signal line crossovers in April and May, but IBM continued trending higher. Even though upward momentum slowed after the surge, it was still stronger than downside momentum in April-May. The third bearish signal line crossover

in May resulted in a good signal.

Centerline Crossovers

Centerline crossovers are the next most common MACD signals.

- A bullish centerline crossover occurs when the MACD line moves above the zero line to turn positive. This happens when the 12-day EMA of the underlying security moves above the 26-day EMA.

- A bearish centerline crossover occurs when the MACD line moves below the zero line to turn negative. This happens when the 12-day EMA moves below the 26-day EMA.

- Centerline crossovers can last a few days or a few months, depending on the strength of the trend.

- The MACD will remain positive as long as there is a sustained uptrend.

- The MACD will remain negative when there is a sustained downtrend.

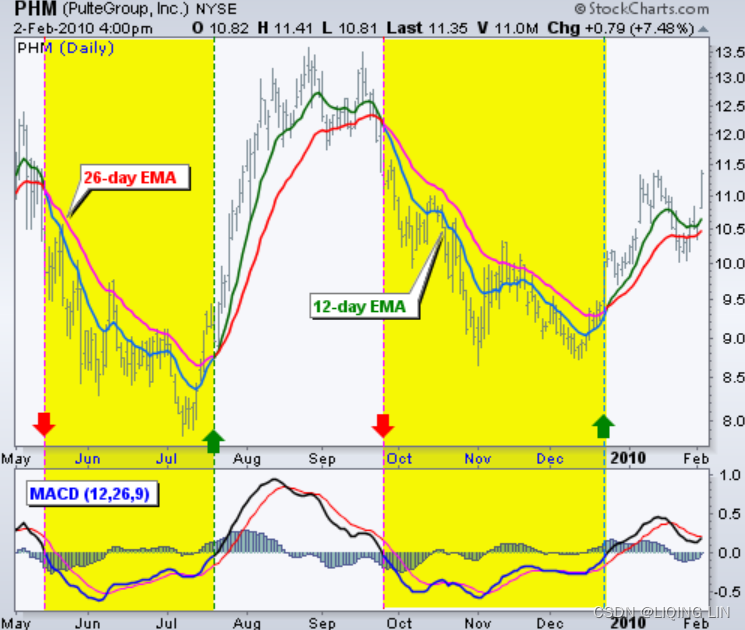

The chart shows Pulte Homes (PHM) with at least four centerline crosses in nine months. The resulting signals worked well because strong trends emerged with these centerline crossovers.

The chart shows Pulte Homes (PHM) with at least four centerline crosses in nine months. The resulting signals worked well because strong trends emerged with these centerline crossovers.

The chart of Cummins Inc (CMI) with seven centerline crossovers in five months. In contrast to Pulte Homes, these signals would have resulted in numerous whipsaws because strong trends did not materialize after the crossovers.与 Pulte Homes 相比,这些信号会导致大量洗盘,因为在交叉之后没有出现强劲趋势。

The chart shows 3M (MMM) with a bullish centerline crossover in late March 2009 and a bearish centerline crossover in early February 2010. This signal lasted 10 months. In other words, the 12-day EMA was above the 26-day EMA for 10 months. This was one strong trend.

The chart shows 3M (MMM) with a bullish centerline crossover in late March 2009 and a bearish centerline crossover in early February 2010. This signal lasted 10 months. In other words, the 12-day EMA was above the 26-day EMA for 10 months. This was one strong trend.

Divergences

Divergences form when the MACD diverges from the price action of the underlying security. A bullish divergence forms when a security records a lower low and the MACD forms a higher low. The lower low in the security affirms the current downtrend, but the higher low in the MACD shows less downside momentum. Despite decreasing, downside momentum is still outpacing upside momentum as long as the MACD remains in negative territory尽管下降,但只要 MACD 仍处于负区域,下行势头仍超过上行势头. Slowing downside momentum can sometimes foreshadow a trend reversal or a sizable rally下行势头放缓有时预示着趋势逆转或大幅反弹.

The chart shows Google (GOOG) with a bullish divergence in October-November 2008.

The chart shows Google (GOOG) with a bullish divergence in October-November 2008.

- First, notice that we are using closing prices to identify the divergence. The MACD's moving averages are based on closing prices and we should consider closing prices in the security as well.

- Second, notice that there were clear reaction lows (troughs) as both Google and its MACD line bounced in October and late November.

- Third, notice that the MACD formed a higher low as Google formed a lower low in November. The MACD turned up with a bullish divergence and the subsequent signal line crossover in early December. Google confirmed a reversal with a resistance breakout.

A bearish divergence forms when a security records a higher high and the MACD line forms a lower high. The higher high in the security is normal for an uptrend, but the lower high in the MACD shows less upside momentum. Even though upside momentum may be less, upside momentum is still outpacing downside momentum as long as the MACD is positive.尽管上行势头可能减弱,但只要 MACD 为正,上行势头仍超过下行势头。 Waning upward momentum can sometimes foreshadow a trend reversal or sizable decline. 上升势头减弱有时预示着趋势逆转或大幅下跌。

we see Gamestop (GME) with a large bearish divergence from August to October. The stock forged a higher high above 28, but the MACD line fell short of its prior high and formed a lower high. The subsequent signal line crossover and support break in the MACD were bearish. On the price chart, notice how broken support turned into resistance on the throwback bounce in November (red dotted line). This throwback provided a second chance to sell or sell short.

Divergences should be taken with caution. Bearish divergences are commonplace in a strong uptrend, while bullish divergences occur often in a strong downtrend. Yes, you read that right. Uptrends often start with a strong advance that produces a surge in upside momentum (MACD). Even though the uptrend continues, it continues at a slower pace that causes the MACD to decline from its highs. Upside momentum may not be as strong, but it will continue to outpace downside momentum as long as the MACD line is above zero.上行势头可能不那么强劲,但只要 MACD 线高于零,上行势头就会继续超过下行势头 The opposite occurs at the beginning of a strong downtrend相反的情况发生在强劲下降趋势的开始.  The chart shows the S&P 500 ETF (SPY) with four bearish divergences from August to November 2009. Despite less upside momentum, the ETF continued higher because the uptrend was strong. Notice how SPY continued its series of higher highs and higher lows. Remember, upside momentum is stronger than downside momentum as long as the MACD is positive.请记住,只要 MACD 为正,上行势头就强于下行势头 The MACD (momentum) may have been less positive (strong) as the advance extended, but it was still largely positive.随着上涨的扩大,MACD(动量)可能不那么积极(强劲),但它在很大程度上仍然是积极的。

The chart shows the S&P 500 ETF (SPY) with four bearish divergences from August to November 2009. Despite less upside momentum, the ETF continued higher because the uptrend was strong. Notice how SPY continued its series of higher highs and higher lows. Remember, upside momentum is stronger than downside momentum as long as the MACD is positive.请记住,只要 MACD 为正,上行势头就强于下行势头 The MACD (momentum) may have been less positive (strong) as the advance extended, but it was still largely positive.随着上涨的扩大,MACD(动量)可能不那么积极(强劲),但它在很大程度上仍然是积极的。

MACD vs. Relative Strength

相对强弱指数 (RSI) 旨在表明市场相对于近期价格水平是否被视为超买或超卖。 RSI 是一个震荡指标,计算给定时间段内的平均价格收益和损失。 默认时间段为 14 个周期,值介于 0 到 100 之间。读数高于 70 表明超买情况,而低于 30 的读数被认为超卖,两者都可能表明顶部正在形成,反之亦然(底部正在形成 ).

然而,MACD 线并没有像 RSI 和其他振荡器研究那样具体的超买/超卖水平。 相反,它们是在相对的基础上发挥作用的。 也就是说,与手头证券的先前价格变动相比,投资者或交易者应关注 MACD/信号线的水平和方向,如下所示。 MACD measures the relationship between two EMAs, while the RSI measures price change in relation to recent price highs and lows. These two indicators are often used together to give analysts a more complete technical picture of a market.

MACD measures the relationship between two EMAs, while the RSI measures price change in relation to recent price highs and lows. These two indicators are often used together to give analysts a more complete technical picture of a market.

这些指标都衡量市场的动能,但由于它们衡量的因素不同,因此有时会给出相反的指示。 例如,RSI 可能会在一段时间内显示高于 70(超买)的读数,表明市场相对于近期价格过度扩张至买方,而 MACD 表明市场的购买势头仍在增加。 任一指标都可能通过显示与价格的背离来预示即将发生的趋势变化(价格继续走高而指标转低,反之亦然)。

Limitations of MACD and Confirmation

移动平均线背离的主要问题之一是它通常可以发出可能的逆转信号,但实际上并没有发生逆转——它会产生误报。 另一个问题是背离并不能预测所有的逆转。 换句话说,它预测了太多没有发生的反转,并且没有足够的实际价格反转。

这表明应通过趋势跟踪指标寻求确认,例如方向运动指数 (DMI) 系统及其关键组成部分平均方向指数 (ADX)。

Plus Directional Movement (+DM)

- Use +DM when current high - previous high > previous low - current low.

if UpMove > DownMove and UpMove > 0,

then +DM = UpMove,

else

+DM = 0 #A negative value would simply be entered as zero

Minus Directional Movement (-DM)

- Use -DM when previous low - current low > current high - previous high.

if DownMove > UpMove and DownMove > 0,

then -DM = DownMove,

else

-DM = 0 #A negative value would simply be entered as zero

Smooth the 14-period averages of +DM, -DM, and TR—the TR formula is below. Insert the -DM and +DM values to calculate the smoothed averages of those.

TR is the greater of the current high - current low, current high - previous close, or current low - previous close.

- First TR14 = sum of first 14 TR

- Second TR14 = First TR14 - (First TR14 /14) + Current TR1

- Subsequent Values = Prior TR14 - (Prior TR14 /14) + Current TR1

Directional Movement Index :

Average Directional Index

- First ADX14 = 14 period Average of DX

- Second ADX14 = ((First ADX14 x 13) + Current DX Value)/14

- Subsequent ADX14 = ((Prior ADX14 x 13) + Current DX Value)/14

import numpy as np

import pandas as pd

def get_adx(df, window=14):

""" get the default setting for Average Directional Index(Average Directional Movement Index)

"""

# +DM = current high - previous high

# -DM = previous low - current low

dm = pd.DataFrame( dict(enumerate([ df['High'] - df['High'].shift(1, fill_value=np.nan),

df['Low'].shift(1,fill_value=np.nan) - df['Low']

])

)

)

# +DM>0 +DM > -DM

df['+dm'] = dm.apply( lambda m: max(m[0],0) if m[0]>m[1] else 0, axis=1)

# -DM>0 -DM > +DM

df['-dm'] = dm.apply( lambda m: max(m[1],0) if m[1]>m[0] else 0, axis=1)

# df['tr']=pd.DataFrame(dict(enumerate([df['High']-df['Low'],

# abs( df['High']-df['Close'].shift(1) ),

# abs( df['Low']-df['Close'].shift(1) )

# ])

# )

# ).apply(max,axis=1)

# OR

df['TrueLow'] = pd.DataFrame(dict(enumerate([ df['Low'],

df['Close'].shift(1),

])

)

).apply( min,axis=1 )

df['TrueHigh'] = pd.DataFrame(dict(enumerate([ df['High'],

df['Close'].shift(1),

])

)

).apply( max,axis=1 )

df.loc[df.index[0],[ 'TrueLow', 'TrueHigh'] ]=np.nan # since df['Close'].shift(1)

# true range

df['tr'] = df['TrueHigh'] - df['TrueLow']

######

df.loc[df.index[0],['+dm', '-dm', 'tr']]=np.nan # for window

def smooth(col):

sm=col.rolling(window).sum()

for i in list( range( window+1,len(col) ) ):

#sm.iloc[i]=sm.iloc[i-1]-(1.0*sm.iloc[i-1]/window)+col.iloc[i]

sm.iloc[i]=col.iloc[i] + (1.0-1.0/window)*sm.iloc[i-1]

return sm

def smooth2(col):

sm=col.rolling(window).mean()

for i in list( range( window*2,len(col) ) ):

#sm.iloc[i]=((sm.iloc[i-1]*(window-1))+col[i])/window

sm.iloc[i]=(1.0/window)*col.iloc[i] + (1-1.0/window)*sm.iloc[i-1]

return sm

df['smoothed +dm'] = df.loc[:,['+dm']].apply(smooth)

df['smoothed -dm'] = df.loc[:,['-dm']].apply(smooth)

df['smoothed tr'] = df.loc[:,['tr']].apply(smooth)

df['+di_{}'.format(window)] = 100.0 * df['smoothed +dm'] / df['smoothed tr']

df['-di_{}'.format(window)] = 100.0 * df['smoothed -dm'] / df['smoothed tr']

df['di_{}_diff'.format(window)]=(df['+di_{}'.format(window)] - df['-di_{}'.format(window)])

df['dx_{}'.format(window)] = 100.0 *abs( df['di_{}_diff'.format(window)] ) /

( df['+di_{}'.format(window)] + df['-di_{}'.format(window)] )

df['adx_{}'.format(window)] = df.loc[:,['dx_{}'.format(window)]].apply(smooth2)

df.drop(columns=['smoothed +dm', 'smoothed -dm', 'smoothed tr',

'+dm', '-dm', 'tr',

'dx_{}'.format(window)

],

inplace=True

)

return df

qqq = pd.read_excel('adx.xlsx',

sheet_name='adx',

header=1,

index_col=1

)

qqq=get_adx(qqq.loc['2009-02-11':'2009-03-25', ['High','Low','Close']],)

qqqADX 旨在指示趋势是否存在,读数高于 25 表示趋势存在(任一方向),读数低于 20 表示没有趋势存在。https://blog.csdn.net/Linli522362242/article/details/129849171

遵循 MACD 交叉和背离的投资者在根据 MACD 信号进行交易之前应仔细检查 ADX。 例如,虽然 MACD 可能显示看跌背离,但检查 ADX 可能会告诉您走高趋势已经到位——在这种情况下,您会避开看跌 MACD 交易信号并等待市场在接下来的时间里如何发展 几天。

另一方面,如果 MACD 显示看跌交叉,而 ADX 处于非趋势区域 (<25) 并且可能已经见顶并自行反转,那么您可能有充分的理由进行看跌交易。

此外,当资产价格在盘整中横向移动时,例如在趋势之后的范围或三角形模式中,经常会出现假阳性背离。 价格势头放缓(横向移动或缓慢趋势移动)将导致 MACD 脱离其先前的极值并趋向于零线,即使没有真正的反转也是如此。 同样,在行动之前仔细检查 ADX 以及趋势是否到位。

Conclusion

The MACD indicator is special because it brings together momentum and trend in one indicator. This unique blend of trend and momentum can be applied to daily, weekly or monthly charts. The standard setting for MACD is the difference between the 12- and 26-period EMAs. Chartists looking for more sensitivity may try a shorter short-term moving average and a longer long-term moving average. MACD(5,35,5) is more sensitive than MACD(12,26,9) and might be better suited for weekly charts. Chartists looking for less sensitivity may consider lengthening the moving averages. A less sensitive MACD will still oscillate above/below zero, but the centerline crossovers and signal line crossovers will be less frequent.不太敏感的 MACD 仍将在零上方/下方振荡,但中线交叉和信号线交叉的频率会降低。

MACD 不是特别适合识别超买和超卖水平。 尽管可以识别历史上的超买或超卖水平,MACD 没有任何上限或下限来约束其走势。 在剧烈波动期间,MACD 可能会继续过度扩张,超出其历史极值。

Finally, remember that the MACD line is calculated using the actual difference between two moving averages. This means MACD values are dependent on the price of the underlying security. The MACD values for a $20 stocks may range from -1.5 to 1.5, while the MACD values for a $100 may range from -10 to +10. It is not possible to compare MACD values for a group of securities with varying prices. If you want to compare momentum readings, you should use the Percentage Price Oscillator (PPO), instead of the MACD.不可能比较一组价格不同的证券的 MACD 值。 如果您想比较动量读数,您应该使用百分比价格震荡指标 (PPO),而不是 MACD。

Divergence Index

Standard deviation, which will be referred to as STDEV, is a basic measure of price volatility that is used in combination with a lot of other technical analysis indicators to improve them. We'll explore that in greater detail in this section.

Standard deviation is a standard measure that is computed by measuring the squared deviation of individual prices from the mean price, and then finding the average of all those squared deviation values. This value is known as variance, and the standard deviation is obtained by taking the square root of the variance. Larger STDEVs are

- a mark of more volatile markets or

- larger expected price moves,

- so trading strategies need to factor that increased volatility into risk estimates and other trading behavior.因此,交易策略需要将增加的波动性纳入风险估计和其他交易行为中。

To compute standard deviation, first we compute the variance:

Then, standard deviation is simply the square root of the variance:

SMA : Simple moving average over n time periods.t2_Deciphering the Market_ticklabels_sma_ewma_apo_macd_Bollinger_Momentum_statsmodels_adfuller_ARIMA_LIQING LIN的博客-CSDN博客

A method similar to MACD but one that uses an interesting combination of generalized techniques is the divergence index, the volatility-adjusted difference between two moving averages, for example, 10 and 40 days. Using general notation:

- 1.

= 40-day average of the most recent prices

- 2.

= 10-day average of the most recent prices

- 3.

Then the divergence index (DI),

The standard deviation of the price differences, taken over the slow period of 40, volatility-adjusts the results. The trading rules require a band around zero to trigger entries.

where factor = 1.0. By using the standard deviation of DI, the band also adjusts to changes in volatility波段还可以根据波动率的变化进行调整. In Figure 9.10 the index in the lower panel has high peaks followed by periods of low or varying volatility. The standard deviation allows the bands to widen or narrow according to the pattern of fluctuations标准偏差允许波段根据波动模式加宽或变窄. This example used the slow period for the standard deviation; however, the fast period would have caused more rapid changes to the band这个例子使用标准差的慢周期; 但是,快速周期会导致波段发生更快速的变化。 FIGURE 9.10 Divergence index applied to S&P futures..

FIGURE 9.10 Divergence index applied to S&P futures..

The trading rules are

- Buy when the DI moves below the lower band while in an uptrend

- Sell when the DI moves above the upper band while in a downtrend

- Exit longs and shorts when the DI crosses zero

Figure 9.10 shows the DI and the upper and lower bands in the bottom panel. The top panel shows the trading signals for the S&P 500 futures contract.

Oscillator

Because the representation of momentum is that of a line fluctuating above and below a zero value, it has often been termed an oscillator. Even though it does oscillate, the use of this word is confusing. In this presentation, the term oscillator will be restricted to a specific form of momentum that is normalized and expressed in terms of values that are limited to the ranges between +1 and –1 (or +100 to –100), +1 and 0, or +100 and 0 (as in a percent).

To transform a standard momentum calculation into the normalized form with a maximum value of +1 and a minimum value of −1, divide the momentum calculation by its range over the same rolling time period. This allows the oscillator to self-adjust to changes in price or volatility.

For example,

- in April 2006, Amazon was trading at about $34. During a 10-day period it had a high of $35.31 and a low of $31.52, a range of $3.79=35.31-31.52.

- During 10 days in February 2011, Amazon had a high of $191.40 and a low of $174.77, a range of $16.63=191.40-174.77.

- Therefore, a price move of $2 in 2006 would be the same as a move of $8.77 in 2011. By dividing $2 by $3.79 or $8.77 by $16.63 we get 0.52 in both cases.

- Hence, normalization, which is the basis for most momentum indicators, can be an excellent way to self-adjust to price changes.

The following sections show how a number of useful oscillators are calculated. In each case, the purpose is to have the indicator post high values when prices are at a peak and low values when they are in a valley. To be most useful, prices should reverse direction soon after the oscillator records values near its extremes.

(RSI-Momentum indicator)Relative Strength Index

One of the most popular indicators for showing overbought and oversold conditions is the Relative Strength Inde(RSI) developed by Welles Wilder. It provides added value to the concept of momentum by scaling all values between 0 and 100. It is more stable than momentum because it uses all the values in the calculation period rather than just the first and last. It is a simple measurement that expresses the relative strength of the current price movement as increasing from 0 to 100. It is calculated as and

The very first calculations for average gain(Average price change on up days) and average loss(Average price change on down days) are simple 14-period averages:

- First Average Gain = Sum of Gains over the past 14 periods / 14.

- First Average Loss = Sum of Losses over the past 14 periods / 14

The second, and subsequent, calculations are based on the prior averages and the current gain loss:

- Average Gain = [(previous Average Gain) x 13 + current Gain] / 14.

- Average Loss = [(previous Average Loss) x 13 + current Loss] / 14

- at least 250 data points prior to the starting date of any chart

import numpy as np import pandas as pd def get_rsi(df, columnName='Adj Close',window=14): # https://pandas.pydata.org/docs/reference/api/pandas.Series.diff.html # Series.diff(default periods=1) # periods=1 : diff = current row - 1st previous row # # periods=3 : diff = current row - 3rd previous row # # periods=-1 : diff = current row - 1st following row df['Up Move'] = df[columnName].diff().apply(lambda diff: diff if diff>0 else 0) df['Down Move'] = df[columnName].diff().apply(lambda diff: -diff if diff<0 else 0) df['Average Up'] = np.nan df['Average Down'] = np.nan # Calculate initial Average Up & Down, RS and RSI # First Average Gain (Average price change on up days) df['Average Up'].iloc[window] = df['Up Move'].iloc[1:window+1].mean() # 1 since df['Up Move'][0] is NaN <== diff() # First Average Loss (Average price change on down days) df['Average Down'].iloc[window] = df['Down Move'].iloc[1:window+1].mean() # 1 since df['Down Move'][0] is NaN <== diff() # Relative Strength df['rs_{}'.format(window)] = np.nan # Relative Strength Index df['rsi_{}'.format(window)] = np.nan df['rs_{}'.format(window)].iloc[window] = df['Average Up'].iloc[window] / df['Average Down'].iloc[window] df['rsi_{}'.format(window)].iloc[window] = 100 - ( 100/(1+df['rs_{}'.format(window)].iloc[window]) ) # Calculate rest of Average Up, Average Down, RS, RSI for row_index in range( window+1, len(df) ): df['Average Up'].iloc[row_index] = (df['Average Up'].iloc[row_index-1]*(window-1) + df['Up Move'].iloc[row_index] )/window df['Average Down'].iloc[row_index] = (df['Average Down'].iloc[row_index-1]*(window-1) + df['Down Move'].iloc[row_index] )/window df['rs_{}'.format(window)].iloc[row_index] = df['Average Up'].iloc[row_index] / df['Average Down'].iloc[row_index] df['rsi_{}'.format(window)].iloc[row_index] = 100 - (100/(1+df['rs_{}'.format(window)].iloc[row_index])) df.drop(columns=['Up Move','Down Move', 'Average Up','Average Down', 'rs_{}'.format(window) ], inplace=True ) return dfAll price changes are treated as positive numbers. The daily calculation of the RSI becomes a matter of simple arithmetic. Wilder has favored the use of 14 days because it represents one-half of a natural cycle, in this case, 1 month. He has set the significant threshold levels for the RSI at 30 and 70.

-

Penetration of the lower level is indicative of an imminent upturn and

-

penetration of the upper level, a pending downturn.

-

A chart of an RSI is shown along with a comparable momentum and stochastic indicator in the next section, Figure 9.15.

-

FIGURE 9.11 RSI top formation.

FIGURE 9.11 RSI top formation.

Use of the RSI alone to generate trading signals often requires interpretation similar to standard chart analysis. Lines are drawn across the tops of the RSI values to indicate a downtrend. A head-and-shoulders formation can be used as the primary confirmation of a change in direction. Wilder himself used the RSI top and bottom formations shown in Figure 9.11. A break of the reaction bottom between the declining tops is a sell signal. In addition, the failure swing, or divergence (discussed later in this chapter), denotes an unsuccessful test of a recent high or low RSI value失败摆动或背离(在本章后面讨论)表示对最近高或低 RSI 值的测试不成功。.

Wilder created other popular indicators. One of these is a momentum calculation called the Average Directional Movement (ADX). The ADX is a byproduct副产品 of the Directional Movement and is discussed in Chapter 23. All of these indicators are actively used by traders.

Modifying the RSI

An obvious objection反对的理由 to the RSI might be the selection of a 14-day half-cycle. Maximum divergence is achieved by using a moving average that is some fraction of the length of the dominant cycle, but 14 days may not be that value. If a 14-day calculation period is too short, then the RSI would remain outside the 70-30 zones for extended periods rather than signaling an immediate turn. In practical terms, a 14-day RSI means that a sustained move in one direction that lasts for more than 14 days will produce a very high RSI value. If prices continue higher for more than 14 days, then the RSI, as with other oscillators, will go sideways. The idea is to pick the calculation period for which there are very few larger sustained moves, and 14 may be that value. If more frequent overbought and over-sold conditions are needed, then the period could be lowered to 10. At the same time, the zones could be increased to 80-20. Some combination of calculation period and zone will usually give the frequency of trades that is needed.对 RSI 的一个明显反对意见可能是选择 14 天半周期。 最大背离是通过使用占主导周期长度的一小部分的移动平均线来实现的,但 14 天可能不是那个值。 如果 14 天的计算周期太短,则 RSI 将长时间保持在 70-30 区域之外,而不是立即转向的信号。 实际上,14 天 RSI 意味着朝一个方向持续移动超过 14 天将产生非常高的 RSI 值。 如果价格持续走高超过 14 天,则 RSI 与其他震荡指标一样将横盘整理。 这个想法是选择几乎没有较大的持续移动的计算周期,14 可能是那个值。 如果需要更频繁的超买和超卖条件,那么周期可以降低到 10。同时,区域可以增加到 80-20。 计算周期和区域的某种组合通常会给出所需的交易频率。

A study by Aan(Peter W. Aan, “How RSI Behaves,”Futures (January 1985).) on the distribution of the 14-day RSI showed that the average RSI top and bottom value consistently grouped near 72 and 32, respectively. Therefore, 50% of all RSI values fall between 72 and 32, which can be interpreted as normally distributed, and equivalent to about 0.675 standard deviations. This would suggest that the 70-30 levels proposed by Wilder are too close together to act as selective overbought/oversold values, but should be moved farther apart. The equivalent of 1.5 standard deviations is a comfortable trade-off between frequency of trades and risk. It is generally safer to err on the side of less risk. If there are too many trades being generated by the RSI, a combination of a longer interval and higher confi dence bands will be an improvement.通常在风险较小的情况下犯错更安全。 如果 RSI 产生的交易太多,则结合使用更长的间隔和更高的置信区间将是一种改进。

Further Smoothing with N-Day Ups and Downs(N日涨跌进一步平滑)

Instead of increasing the number of days in the RSI calculation period, a smoother indicator can be found by increasing the period over which each of the up and down values are determined. 与其增加 RSI 计算周期中的天数,不如通过增加确定每个上升值和下降值的周期来找到更平滑的指标。The original RSI method uses 14 individual days, where an up day is a day in which the price change was positive. Instead, we can replace each 1-day change with a 2-day change, or an n-day change. If we use 2-day changes, then a total of 28 days will be needed, so that each 2-day period does not overlap another; there will be 14 sets of two days each. Using 14 sets of 2 will give a smoother indicator than using 28 single-day changes.

RSI Countertrend Trading

Momentum indicators are used for timing and countertrend trading. Normally, it is the absolute overbought or oversold level that is the trigger for a trade. However, either a very fast move in price or an extreme value for a momentum indicator could be a criterion for a reversal. When , or when

, where

is a threshold value, we could sell and buy, respectively. This also increases the number of trades because it does not require that

, only that it has moved quickly. Exits can be taken when momentum returns to near zero, or after n days. A program to test this is TSM RSI Countertrend, available on the Companion Website.

{ TSM RSI Countertrend

Copyright 2012, P.J.Kaufman. All rights reserved.

Buy when the RSI momentum is oversold;

Sell when overbought;

exit after n days or at zero RSI

}

inputs: period(9), momperiod(5), exitdays(3), buylevel(-15), selllevel(15);

vars: mom(0);

mom = RSI(close,period);

if marketposition <> 1 and mom - mom[momperiod] < buylevel

then buy 1 contract next bar on open

else if marketposition <> -1 and mom - mom[momperiod] > selllevel

then sell 1 contract next bar on open;

if barssinceentry >= 3

then begin

if marketposition = 1

then sell all contracts next bar on open

else if marketposition = -1

then buy to cover all contracts next bar on open;

end;

if marketposition = 1 and mom > 50

then sell all contracts next bar on open

else if marketposition = -1 and mom < 50

then buy to cover all contracts next bar on open; Net Momentum Oscillator

Another variation on the RSI is the use of the difference between the sum of the up days and the sum of the down days, called a net momentum oscillator. If you consider the unsmoothed then the net momentum oscillator would be

This method replaces some of the indicator movement lost to smoothing in the normal RSI, and shows more extremes. This may also be done by shortening the number of periods in the RSI calculation.此方法取代了正常 RSI 中因平滑而丢失的一些指标移动,并显示了更多的极端情况。 这也可以通过缩短 RSI 计算中的周期数来完成

The 2-Day RSI

Among the interesting information published on MarketSci Blog 8 is Michael Stokes’s “favorite” indicator, the 2-day RSI, which replaces each 1-day change with a 2-day change; otherwise, the calculations and the number of data points are the same. If you already have a program to calculate the RSI, you only need to change the statement with

to get overlapping 2-day data. Or, to try an n-day RSI, replace the “2” with your choice of days. The effect of using combined 2 days instead of 1 is some smoothing and a general increase in volatility.使用组合 2 天而不是 1 天的效果是一些平滑和波动性的普遍增加。

Stokes uses threshold levels of 10 and 90 for the S&P and the rules

- Buy on the next close when the 2-day RSI penetrates the threshold of 10 moving lower

- Sell short on the next close when the 2-day RSI penetrates the threshold of 90 moving higher

- Exit one day later on the close 一天后收盘退出

FIGURE 9.12a Performance of the 2-day RSI, MarketSci blog’s favorite oscillator, from the December 9, 2008, posting, simple entries <10 and >90 applied to the S&P, 1970 through 2008.

FIGURE 9.12a Performance of the 2-day RSI, MarketSci blog’s favorite oscillator, from the December 9, 2008, posting, simple entries <10 and >90 applied to the S&P, 1970 through 2008.

Figures 9.12a and b are from the MarketSci Blog on December 9, 2008.

- Figure 9.12a shows that the profitability of the RSI reversed in about 1998. From 1970 to 1998 it was a good trend indicator; that is, when the RSI moved above 90 the S&P continued up. After 1998 it has been a much better mean-reverting indicator.

从 1970 年到 1998 年,它是一个很好的趋势指标; 也就是说,当 RSI 升至 90 上方时,标准普尔继续上涨。 1998 年之后,它成为一个更好的均值回归指标 - Figure 9.12b is the result of applying a method of scaling in to trades according to the following rules:

FIGURE 9.12b A breakdown of longs and short sales using the scaling-in method, S&P 2000 through 2008.

FIGURE 9.12b A breakdown of longs and short sales using the scaling-in method, S&P 2000 through 2008.

On day t the RSI was 14 (<15), and we entered 50%, but then on day t + 1 the RSI dropped to 8; it was not clear whether we added an extra 25%, but we assume that is the case. Then the trade is exited if we do not add on the next day. Because the RSI can stay above or below 50 for long periods of time, an exit rule that waits for the RSI to cross 50 is not likely to be successful. Stokes’s approach of exiting after one day seems much safer. Figure 9.12b separates the longs and short sales from 2000 through 2008, showing that both sides performed well, a very desirable outcome. Having good performance for longs and shorts is not common because many markets have an upwards bias (especially the stock market). However, 1-day trades are sensitive to costs. Traders will need to see if the returns per share, or per contract, are suffi cient to cover commissions and slippage.

在 t 日,RSI 为 14,我们进入 50%,但随后在 t+1 日,RSI 降至 8; 目前尚不清楚我们是否额外增加了 25%,但我们假设是这样。 如果我们不在第二天添加,那么交易将退出。 由于 RSI 可以长时间保持在 50 以上或以下,因此等待 RSI 超过 50 的退出规则不太可能成功。 Stokes 在一天后退出的方法似乎更安全。 图 9.12b 将 2000 年至 2008 年的多头和空头销售分开,表明双方都表现良好,这是一个非常理想的结果。 多头和空头都有良好的表现并不常见,因为许多市场都有向上的偏见(尤其是股市)。 然而,1 日交易对成本很敏感。 交易者需要查看每股或每份合约的回报是否足以支付佣金和滑点。

A Standard 2-Period RSI

FIGURE 9.13 2-Period RSI (center panel) compared with the traditional 14-day RSI (bottom panel), applied to NASDAQ futures, August 2005 through September 2008.

FIGURE 9.13 2-Period RSI (center panel) compared with the traditional 14-day RSI (bottom panel), applied to NASDAQ futures, August 2005 through September 2008.

In Figure 9.13 a standard 2-period RSI is shown in the middle panel and the traditional 14-day RSI in the lower panel. Both are applied to NASDAQ futures, from August 2005 through September 2008, which appears at the top.

- The classic RSI penetrates the extremes of 30 and 70 but does not reach 20 or 80,

- while the 2-period RSI touches near 15 and 85 a number of times.

We might expect a 2-period oscillator to jump between 0 and 100 every day that prices changed direction, but the average-off calculation slows down the process and makes the 2-period chart a somewhat more volatile version of the standard RSI.

slows down the process and makes the 2-period chart a somewhat more volatile version of the standard RSI.

在图 9.13 中,标准的 2 周期 RSI 显示在中间面板中,传统的 14 天 RSI 显示在下面板中。 两者都适用于从 2005 年 8 月到 2008 年 9 月出现在顶部的纳斯达克期货。 经典 RSI 突破 30 和 70 的极端,但没有达到 20 或 80,而 2 周期 RSI 多次触及 15 和 85 附近。 我们可能期望 2 周期震荡指标每天在价格改变方向时在 0 和 100 之间跳跃,但average-off calculation减慢了该过程并使 2 周期图表成为标准 RSI 的更具波动性的版本。

An RSI Version of MACD

While the MACD creates a histogram of the difference between two moving averages, we can make that pattern easier to interpret by applying the RSI to the spread of the moving averages. In Figure 9.14 a 5-day RSI is applied to the difference between the 10- and 40-week moving average for the emini-S&P futures. Using the standard 30-70 thresholds, this seems to find credible points where prices are overbought and oversold.  FIGURE 9.14 RSI applied to the spread between a 10-week and 40-week moving average of

FIGURE 9.14 RSI applied to the spread between a 10-week and 40-week moving average of

S&P futures.

Stochastics - momentum indicator

The stochastic indicator, created by George Lane, is an oscillator that measures the relative position of the closing price within a past high-low range. It is based on the commonly accepted observation that closing prices tend to resist penetrating the high prices of the past few days, the place where a horizontal resistance line would be drawn on a chart.它基于普遍接受的观察结果,即收盘价往往难以突破过去几天的高价,即图表上绘制水平阻力线的位置。 Similarly, in a downtrend prices must be able to close below the lows of the past few days for the move to continue. When the market is about to turn from up to down, for instance, it is often the case that the highs are higher than previous days, but the closing price settles nearer the low of the day, failing to indicate a continuation of the uptrend. This makes the stochastic oscillator different from the MACD, which uses the difference between two trends(2 EMA), and the RSI which uses only the closing prices. The stochastic uses the high, low, and close and unlike the other oscillators, there does not have to be any smoothing to introduce a lag.